-

Legal EditorHenry Dahut, J.D.

Henry Dahut, J.D.

Founder

Henry Dahut is a licensed California trial attorney. Over the course of his 30-plus years practicing law, Henry has represented and counseled countless clients in legal trouble.

Read more → -

This article covers how personal injury settlements are paid out, including the types of payments, legal documentation, distribution of funds, tax implications, and the role of personal injury attorneys.

What are Personal Injury Settlements?

Personal injury settlements are agreements reached between an injured party and the party responsible for the injury, usually through their insurance company.

The great majority of personal injury lawsuits are settled before going to trial. Settlements usually occur shortly before or after a lawsuit is filed or just before trial.

Because of the inherent uncertainty of jury trial results, there can be significant benefits to settling your personal injury case at the mediation or settlement conference stage.

About This Article

This article covers the settlement process in personal injury cases, including the role and responsibilities personal injury lawyers take in the settlement process.

You will also learn about the risks of going to trial and the benefits of settlement through mediation or through a court settlement conference.

This article also includes topics such as:

- Common Misconceptions of The Settlement Process

- Why Jury Verdicts Can Be Unpredictable

- Advantages and Disadvantages of Structured Settlements

- Settlement Through Minors Compromise

- The Legal, Financial, and Health Risks of Settling Too Early

Settlement and Personal Injury Lawyers

Experienced personal injury attorneys not only advocate for your rights while navigating the complexities of the litigation process, but they are also experts in facilitating the negotiation process and maximizing settlements.

Having a good idea of your jurisdiction’s average personal injury settlement range is often a reliable guide in providing a realistic estimate of what your case might settle for. However, actual figures can vary widely based on the specifics of each case.

In addition to covering the cost of medical care, personal injury settlements often include compensation for pain and suffering damages.

Financial Tip

Three Common Misconceptions About Personal Injury Settlements

Misconception #1: Pre-existing conditions don’t affect the settlement.

Reality: Insurance companies will try to reduce the settlement by claiming that some or all of the plaintiff’s injuries resulted from an unrelated previous accident, injury, or medical condition and, therefore, cannot be considered compensable damages in the current accident.

Misconception #2: Personal injury settlements are tax-free.

Reality: While some portions of a personal injury settlement, such as compensation for medical expenses or pain and suffering, may be tax-exempt, other parts, like lost wages, may be taxable.

Misconception #3: The settlement process is usually quick and straightforward.

Reality: Personal injury cases can be complex, and the settlement process may involve lengthy negotiations and even litigation. Reaching a final agreement can take months or even years.

Misconception #4: You don’t need a lawyer to settle your personal injury claim.

Reality: While handling a claim without a lawyer is possible, having legal representation can, if your claim is sufficiently large enough and there is sufficient insurance to cover the claim, improve your chances of a higher favorable recovery with legal representation than without.

Misconception #5: The more serious the injuries, the higher the settlement.

Reality: Not always. Settlements are influenced by various factors, including shared liability, insurance coverage, pre-existing injuries, and your attorney’s experience and negotiation skills.

Three Common Misconceptions On How Personal Injury Settlements Are Paid Out

Misconception #1: Settlement payments are always made in a lump sum.

Reality: Settlements can be paid as an upfront lump sum or through a structured settlement such as an annuity, where payments are made over time. This can sometimes depend on the settlement amount, the plaintiff’s age, and current circumstances. It is often best to have your lawyer contact an annuity expert to help you decide whether a structured settlement will be in your best interests.

Misconception #2: You will receive your settlement money as soon as the case settles.

Reality: It can take time to receive the settlement check from the insurance company, as there may be delays in processing. Once the check is received, the entire settlement amount is deposited into your lawyer’s trust account, pending the deduction of legal fees, costs, and medical liens asserted against the case, which is often negotiated and reduced before the settlement funds are dispersed.

Misconception #3: Insurance companies pay settlements directly to the claimant.

Reality: If you are represented by counsel, the full settlement amount is paid to your attorney first, who then disburses the funds to cover fees, costs, and liens. The remaining amount is then issued to the plaintiff.

Settlement Verses Facing an Unpredictable Jury at Trial

Why Are Jury Verdicts Unpredictable?

No one can predict a jury’s actions under a given case’s specific facts and circumstances. This is the primary reason to consider settling your injury case once the discovery phase of your case has concluded.

Every type of personal injury case has its strengths and weaknesses. For example, jurors treat multi-car accidents differently than single-car collisions due to the driver’s cognitive impairment by alcohol or drugs. Proving liability in accidents involving trips and falls can sometimes be more complicated than proving medical malpractice cases. Juries will often treat cases involving strict liability in defective drug cases differently than those of strict liability cases involving a child being attacked by a neighbor’s dog.

Even the most compelling cases can result in a defense verdict or being awarded a sum that is far less than you expected. The reason? Juries tend to view the facts of a case through their own experiences, which may lead to bias and, at times, even resentment, even though the lawyers and judges in personal injury trials do everything they can to eliminate biased jurors from serving on a case.

Juries Can Be Resentful

Conventional wisdom, especially during difficult economic times, is that jurors may also be struggling financially and factor their own frustration into their decision on how much to award the plaintiff—especially when awarding compensation for pain and suffering.

Getting caught up in our financial struggles is easy, especially at trial. As a plaintiff, however, you don’t want to give the jury the impression that you are overreaching on the value of your case, nor do you want to appear over-deserving in the amount you are asking the jury to consider awarding you.

The bottom line is that jury duty is not easy, and much is being asked of them while serving in this capacity.

Your Lawyer Is There to Guide You on Settlement Decisions

Although experienced personal injury lawyers can advise you about the overall strength of your claim and your chances of recovery at trial, jury verdicts are still unpredictable. They may not decide in your favor – no matter how strong or compelling you believe your case to be.

Legal Tips:

What Are the Benefits of Settling Your Case Through Mediation?

As the actual trial date approaches and after a plaintiff has, in most cases, waited a year or more to have their day in court, it is only natural for them to imagine what going to trial might mean and how the trial process might unfold.

The plaintiff might envision a trial filled with high drama and moments of glory, culminating in a public victory and vindication of the plaintiff’s rights. So, you can imagine the disappointment felt when the plaintiff learns their very public case has been ordered to mediation rather than trial.

How Does the Mediation Process Work?

Depending on the jurisdiction and the amount of money the plaintiff claims in damages, almost all personal injury cases are sent to mediation before trial. Some jurisdictions may refer to this process as a settlement conference. However, there are differences:

Differences Between Mediations and Court-Ordered Settlement Conferences

Mediation is usually a voluntary, confidential process in which the parties meet with a neutral, outside third-party mediator to reach a settlement. The opposing parties split the mediator’s fee. Mediations can be highly structured, lengthy, and expensive.

Settlement Conferences are usually ordered by the court shortly before trial. They often take the form of meetings at the courthouse, where the parties and their attorneys meet with a judge or local lawyer who acts as a neutral third party to help them settle their case.

Some jurisdictions may charge the parties a minimal fee for the conference.

However, both forms of settlement forums, whether voluntary or involuntary, share the same purpose – settlement of the case.

In both situations, the opposing lawyers present their case to a neutral third person who tries to convince the parties to settle. This usually involves an uncomfortably long and tedious process in which the neutral instills fear in both parties about the fundamental risks of going to trial.

(Above Image) Image showing the difference between a plaintiff receiving a settlement as a lump sum payment versus a structured settlement.

What Are Structured Settlements?

Structured Annuities

In personal injury cases in which the plaintiff settles for large sums of money, the plaintiff’s counsel will likely discuss the option of receiving their settlement over time instead of receiving it in a lump sum payment now. This is often referred to as a structured settlement.

Cases Involving Minors as The Plaintiff

The Minors Compromise

A court-ordered minor’s compromise is a mandatory legal procedure in which the court reviews the proposed settlement to ensure its fairness. The judge will consider factors such as the severity of the injury, the potential long-term effects on the minor, and the adequacy of the compensation offered.

Sometimes, the court may appoint an independent guardian at litem to represent the minor’s interests regarding the proposed settlement. This person will investigate the circumstances of the case and make recommendations to the court based on the minor’s best interests.

In many states like California, the plaintiff’s attorney fees are limited by law to 25% of the net settlement.

Usually, the court will set up a hearing. At this hearing, the judge can ask questions and hear testimony from the lawyers, the minor, and any other relevant parties, such as the minor’s parents or caretakers.

If the judge determines at the hearing that the settlement is in the minor’s best interest, the court will issue a court order approving the settlement.

This order will specify how the settlement monies should be handled. One option is to place the funds in a blocked account or trust until the minor reaches the age of majority, which is 18 in most jurisdictions.

Structured Settlements for Minors

For minors in personal injury cases, a structured settlement usually provides periodic payments over a specified period rather than a lump sum payment.

This type of settlement is designed to ensure that the minor’s financial needs are met over time, often extending into adulthood.

In summary, the court process involving minors protects minors from potentially unfair or insufficient settlements. It ensures that any compensation they receive is managed wisely.

Watch this video by Amicus Settlement Planners to learn about structured settlement cases involving minors:

More on Structured Settlements

The Periodic Payment Settlement Act of 1982 amended the Federal tax code to recognize and encourage structured settlements in personal injury cases.

Given the legal and financial complexity surrounding structured settlements, the states and the federal government have enacted important consumer legislation and industry regulations to afford more protections for minors.

What Are the Advantages of Structured Settlements?

- Receiving periodic payments can reduce taxes. People choose a structured settlement to avoid the potential tax consequences of a lump sum settlement.

- Receiving periodic payments can also reduce the chance of overspending and running out of money before the next payment arrives.

- A significant advantage to structured settlements is that they can be devised in various ways based on the claimant’s medical needs and specific financial preferences.

These preferences can include periodic payments to the claimant when funds are required for:

- Continued medical expenses

- Continued education

- Vocational education

- Housing expenses

- Continued financial support

Both defense counsel and the insurance company prefer working with annuities because it is far easier for the parties to settle big-dollar cases. One reason is that the settlement amounts can look much larger over time.

Financial Tip

Wellness Tip

The following video explains Structured Settlement Versus the Fixed Income Annuity:

What Are the Disadvantages of Structured Settlements?

- Some claimants under a periodic payment schedule often consider their arrangement unnecessarily restrictive.

- It is tough to change the structure of the agreement once the annuity is locked into place.

- Finally, beware of excessive commissions in structured settlements. Commissions can always be negotiated. A great deal of money is made selling annuities. Ensure the commissions don’t consume too much of the principal. Check with at least two other brokers and your financial advisor before you agree to accept the annuity settlement.

Risks of Settling Your Case Too Early

Legal Risk of Settling Too Early: (Future Claims) Early settlements often require the injured party to sign a release of liability, which means they cannot pursue further legal action related to the injury in the future. This can be problematic if additional complications or costs arise later.

Financial Risk of Settling Too Early: Early settlement can often mean you will be leaving settlement money on the table. Many personal injury lawyers say the best settlement offer will be made just before the trial commences.

Settling Too Early Can Be Bad for Your Physical and Emotional Health: In some cases, plaintiffs may feel pressured to accept a quick settlement offer before fully recovering. This can result in them foregoing necessary care or rehabilitation, which can have long-term consequences on the plaintiff’s health and well-being.

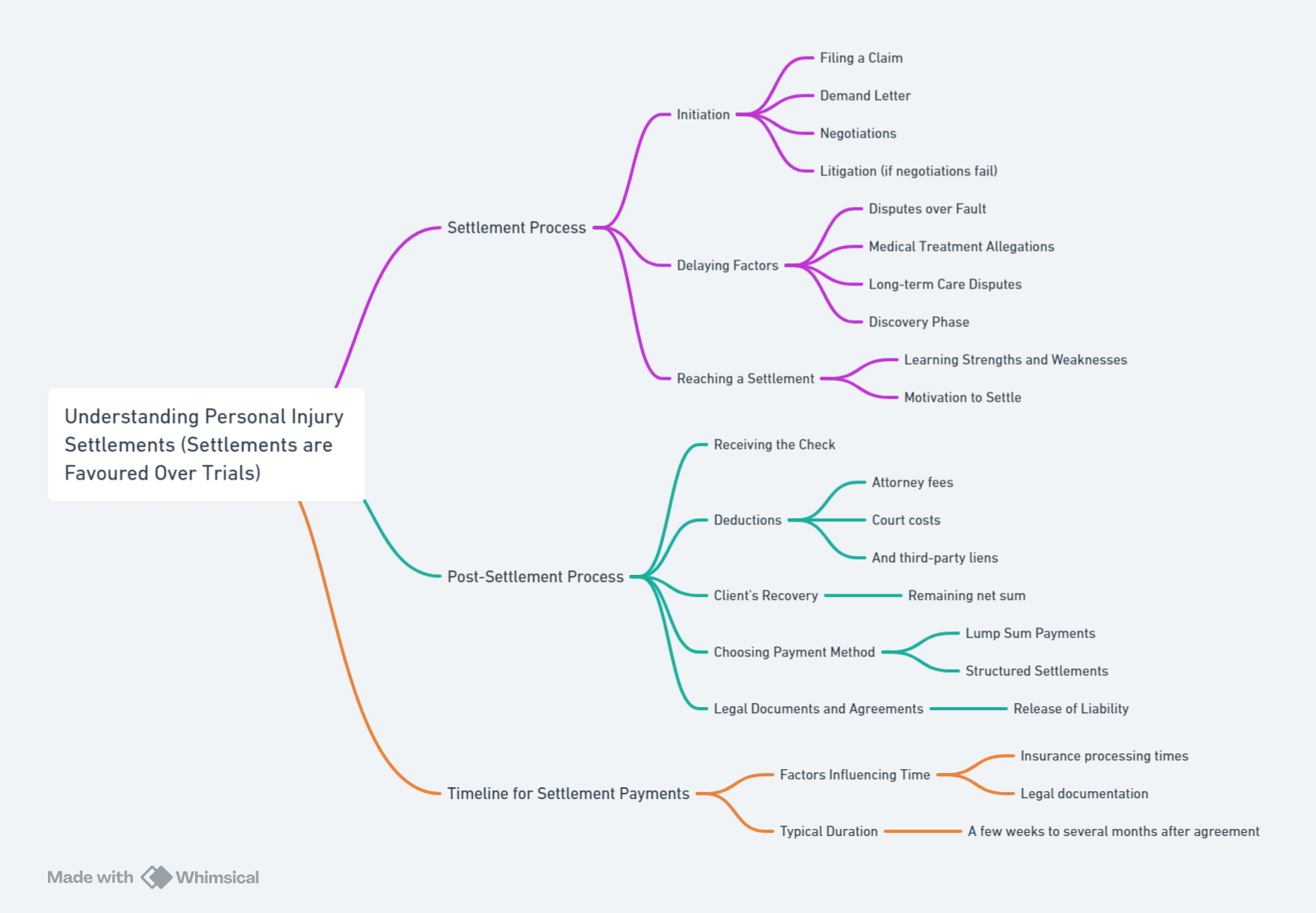

(Above Illustration)Infographic illustrating the phases, duration, factors, and processes involved in personal injury settlements and payouts.

The Bottom Line

- Settlement vs. Trial: Settling a personal injury case through mediation can save time, reduce costs, and provide a more predictable outcome than going to trial.

- Unpredictable Juries: Jury decisions are unpredictable, influenced by personal biases and economic conditions, making settlements a safer option.

- Mediation Benefits: Mediation is informal, confidential, faster, and less expensive than a trial. It allows parties to control the settlement outcome.

- Structured Settlements: They can offer tax benefits and help manage settlement funds over time. However, they can be inflexible and have high fees.

- Importance of Professional Advice: Consulting with a personal injury lawyer and financial planner is crucial to navigating the complexities of settlements and ensuring the best possible outcome.